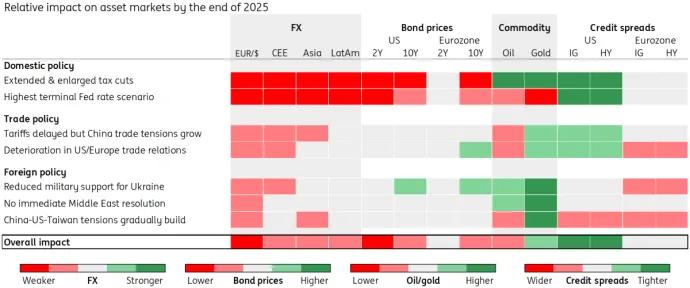

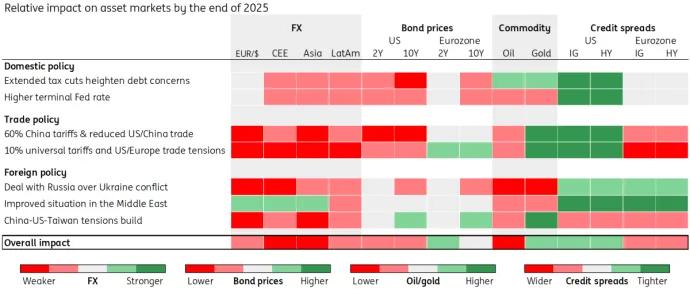

US presidential election: Three scenarios for markets

15 August 2024

Reading time: 4 min

No one can predict what's going to happen on 5 November when Americans go to the polls to elect either Donald Trump or Kamala Harris. The next president of the United States and the parties that will control Congress will have a major say in where financial markets head over the coming years. So, just what might happen to FX, Rates, Commodities, and Credit Markets whoever wins? We have tried to look at various scenarios which could affect asset classes via domestic, foreign and trade policy.

Scenario 1: Trump clean sweep

If Donald Trump wins the Presidency and Republicans win control in Congress, we might witness the following plot:

Macro impact

| Growth | Inflation | Central banks |

|---|---|---|

| Confirmation of tax cuts may give growth an earlier lift while encouragement of reshoring keeps the momentum strong. Tariffs come in later, meaning less immediate pressure on Eurozone. | Tax cuts support domestic demand and immigration controls lift wages marginally, which keep inflation more elevated. Eventual tariffs further lift inflationary pressures. | Stronger growth and higher inflation likely mean Fed keeps interest highest in this scenario. Moreover, ongoing loose fiscal policy is likely to result in tighter monetary policy in general. |

Market impact

| FX | A Republican clean sweep is the most bullish scenario for the dollar medium term. Loose fiscal, tight monetary policy plus tariffs are all positive. Dollar strong, then stronger is our call. |

|---|---|

| Rates | A risk-on theme, whether justified or not, will reduce the bid for bonds, pushing yields up. A gung-ho attitude to the ballooning fiscal deficit adds to issuance, pressuring rates higher. |

| Credit | Strong performance of USD credit back towards the bottom end of trading range, perhaps reaching tights in 2Q25 but ending next year at 120bp. USD outperforms EUR, but no major weakness in EUR. |

| Commodities | Tax cuts support oil prices in short term. Focus on US energy independence and pressure on OPEC+ to increase supply sees weaker prices longer term. Key upside risk is stricter sanction enforcement against Iran. |

Scenario 2: Trump constrained

Provided that Donald Trump wins the Presidency, but Congress split (Democrats win Senate, Republicans win House), we might experience:

Macro impact

| Growth | Inflation | Central banks |

|---|---|---|

| Negligible impact on 2025 US growth given policy constraints but 2026/27 higher on tax cuts/reshoring. Eurozone growth impact slightly negative. | Tax cuts plus tariffs & tighter labour supply (lower immigration) offer modest boost in 2026. | Higher inflation limits Federal Reserve rate cuts. Weaker growth doesn’t accelerate ECB rate cuts given slightly higher inflation. |

Market impact

| FX | Early Trump focus on foreign policy can see USD stronger mid 25 than under a clean sweep. Net-net, a Trump administration is USD +ve. But if US growth falters, weak USD policy is a risk. |

|---|---|

| Rates | The biggest hit to bonds here comes from the tariff war's effect on inflation. This is partially cushioned by the added tax revenue that can be deployed to help reduce the fiscal deficit. |

| Credit | Decent USD performance but less considerable, and more of a slower tightening over the year to also end at 120bp. Expect more outperformance over EUR as EUR credit could see some weakness. |

| Commodities | Early focus on foreign policy sees easing tension in the Middle East weigh on oil prices. Pressure on Russia/Ukraine to come to a deal puts further downward pressure on prices through 2025. |

Scenario 3: President Harris

Assuming that Kamala Harris wins the Presidency, but Congress is split (Democrats win Senate, Republicans win House), we might observe:

Macro impact

| Growth | Inflation | Central banks |

|---|---|---|

| Somewhat tighter fiscal policy will be a headwind to growth, but a more certain trade and economic backdrop may mitigate this, particularly if the Fed feels content with a lower inflation profile. | Some fiscal restraint will help dampen price pressures relative to Trump. Limited migration & trade impact should also lesson inflation fears over the medium term. | A tighter fiscal environment, coupled with modestly weaker growth and reduced inflation threat may see the Fed be more willing to run looser monetary policy relative to the Trump scenarios. |

Market impact

| FX | Somewhat tighter fiscal and looser monetary mix – plus less aggressive trade policy – is a USD negative. Dollar can weaken into year-end and further into 2025 if Fed takes rates down to 3.50%. |

|---|---|

| Rates | Rates are lower because of tighter fiscal response, which facilitates lower rates along the yield curve. A moderately weaker activity backdrop pushes in the same direction. |

| Credit | Some weakness in USD spreads as taxation on corporates adds pressure. Spreads slowly leak wider through the year. EUR credit may see some outperformance over USD credit. |

| Commodities | Lower growth prospects weigh on oil, short term. Middle East tension persists. No Russia/Ukraine deal means oil ends 2025 higher versus other scenarios. Looser monetary policy supports prices in 2025. |

Curious to find out more? Discover further on Opens in a new tabING THINK.