ING Sustainable Finance Pulse - issue 2

27 March 2025

Reading time: 6 min

Welcome to the second issue of ING’s Sustainable Finance Pulse, a quarterly glimpse into the world of sustainable finance and ING’s take on it.

Sustainable finance market

Despite seeing a slowdown in ESG issuance last year, 2024 started on a positive note with the return of an average growth in the market, driven largely by the issuance of green bonds.

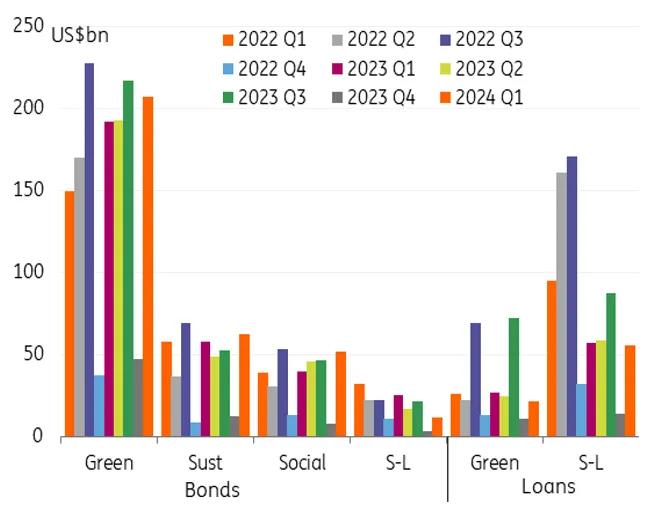

In the first three months of 2024, global ESG issuance reached US$409bn. This is up slightly from the quarterly average since 2021 and up from the past two year’s quarter 1 figures which both came just shy of US$400bn. A large driver of this increase has been on the bond side, rather than the loan issuance side. In the first three months global green bond issuance reached US$207bn. This is just marginally short of the six-month average of US$222bn seen since 2018. This is also up significantly from the US$160bn quarterly average since 2021.

Similarly, global sustainability bond supply has already reached US$62bn, above the quarterly average of US$48bn. Lastly, global social bond supply totalled US$52bn thus far, compared to the USD$42bn quarterly average. The global sustainability-linked bonds, global green loans and sustainability-linked loans are all still at much lower levels than the quarterly averages seen since 2021.

Global issuance of sustainable finance per Quarter

The main driver of the increase in ESG bond issuance is related to overall bond issuance increase. Very substantial, often record-breaking levels of issuance are observed in most currencies and most products. As the rates and macro environment remains stable, the higher yield in credit keeps demand very high, whilst risks and uncertainty still loom for the second half of the year, for instance around upcoming elections in the US. These circumstances are driving significant front loading of issuance to this first quarter of the year

Despite this positive start to the year, global issuance volumes in 2024 are still expected to continue to be lower than previous years and likely to be similar to the volumes seen in 2023, as a slow second half of the year is expected.

We forecast a global ESG bond supply of around €1tr for 2024. According to our ING estimates which takes a slightly smaller universe (of min €250m size and only self-labelled bonds), we expect sovereigns, supranationals, agencies, financial institutions and corporates issuing ca €325 billion in EUR. We expect the USD market to stay stable at €225 billion (US$240 billion). For ESG bonds in other currencies, we expect a soft growth from €260 billion to €270 billion. More specifics of our forecasts can be found in our report - Opens in a new tabGlobal ESG Bond Supply Outlook: Slowing down in 2024.

Global issuance of sustainable finance per product

Deal Highlight

ING is very proud of its leading role in the financing of five battery gigafactory blocks across France, Germany and Italy, built and owned by Automotive Cell Company (ACC), which is a joint venture between car giants Stellantis (makers of cars including Citroën, Fiat, Chrysler and Alfa Romeo among others), Mercedes Benz and Saft, a wholly owned subsidiary of TotalEnergies. Once operational, these factories will produce the batteries that will go into electric vehicles.

ING, together with three other banks, acted as underwriter of this €4.4 billion transaction. The Sustainable Value Chains team was able to bring ING specialists together working closely with colleagues in the Netherlands, Germany, France and Italy, working across the energy, transportation, logistics & automotive, financial markets and structured export finance teams.Want to know more about ING’s Sustainable Value Chains team? Contact Opens in a new tabTim.van.Pelt@ing.com

ING sees busy start of the year

Despite the slowdown in the market last year, ING achieved a strong start to the year, also mostly driven by strong activity in green loans and bonds. ING achieved a volume mobilised of €24.7 billion, an increase of 13% compared to the same period last year. We closed in total 156 sustainability transactions.

Most of ING’s sustainable finance activity was in EMEA (ca 70%), with sustainable finance transactions in APAC also still growing. Despite a volatile market in the Americas, we managed to keep volumes relatively stable in the US, primarily fuelled by green bonds, although volumes are still at historical lows.

Sustainability-linked structures are the outlier in terms of volume growth, in EMEA and Americas, whereas in APAC sustainability linked loans still showed growth in line with market growth. Lower activity in general is logically linked to increased regulatory scrutiny and for the Americas in particular by uncertainty in the political environment.

ING continued to perform strong in the first quarter across the various sustainable finance products. Similar to markets overall we saw particular strong activity in the bond market and a more subdued volume on the lending activity.

Jacomijn Vels, ING’s global head of sustainable finance

Jacomijn Vels also claimed that the outlook for the remainder of the year remains hard to predict. Not only because of general economic or geopolitical uncertainties but also because the deal structuring process often has become more time consuming and complex because of increased scrutiny from regulators.

ING SF transactions

ING Research highlight: Taxonomy Disclosures

For the first time, financial institutions disclosed their EU Taxonomy (EUT) including both eligibility and alignment to the Taxonomy for the year 2023. Banks’ annual reports and Pillar III disclosures now also include the new and widely discussed Green Asset Ratio (GAR), designed to become a snapshot of banks’ environmental sustainability. While some expected this first year’s GAR average to be lower than 10%, banks reported, on average, only 3% GAR. Looking at the EUT eligibility rate however, financial institutions still reported around 35% Taxonomy eligible assets, a 5-percentage point (pp) increase since 2022. These results are derived from a sample of 33 European banks from 13 jurisdictions, and while we note some national variations, results are still strikingly low.One could stress that these very low results show the overall lack of green activities in the European economy or the financial sector’s inaction against climate change. However, according to ING Research other factors are at play that influence both the Taxonomy and GAR results. In this piece, ING Research looks into variables considered in the EUT and Green Asset Ratio calculations, dives into the different methodologies used by banks and their effect on the reported results and summarises this year’s disclosures. Finally, the three main points that could negatively affect results are discussed. Read more Opens in a new tabhere.

Society is transitioning to a low-carbon economy. So are our clients, and so is ING. We finance a lot of sustainable activities, but we still finance more that’s not. See how we’re progressing on ing.com/climate.

Authors

Jacomijn Vels

Global Head of Sustainable Solutions Group

Tim van Pelt

Sustainable Value Chains ING

Marine Leleux

Sector strategist, Financials (Taxonomy Disclosures), ING Research

Timothy Rahill

Credit strategist (Sustainable finance markets), ING ResearchEmail: Opens in a new tabTimothy.Rahill@ing.com

Astrid Overeem

Global PR manager Wholesale BankingEmail: Opens in a new tabAstrid.Overeem@ing.com

You might be also interested in:

Sustainable finance issuance was slightly slower in Q2 this year (2024), despite a rather active Q1. Global sustainable issuance totalled US$376bn in Q2 2024, which is lower than the average of a little over US$400bn seen in Q2 in the past few years. However, looking at global H1 issuance, pencilled in at US$815bn, this is in line with half year levels of the past few years.

ING Sustainable Finance Pulse - issue 3

ING Sustainable Finance Pulse - issue 3