ING Sustainable Finance Pulse - issue 4

31 December 2025

Reading time: 6 min

Welcome to ING’s Sustainable Finance Pulse, a quarterly glimpse into the world of sustainable finance and ING’s take on it.

Sustainable finance market update

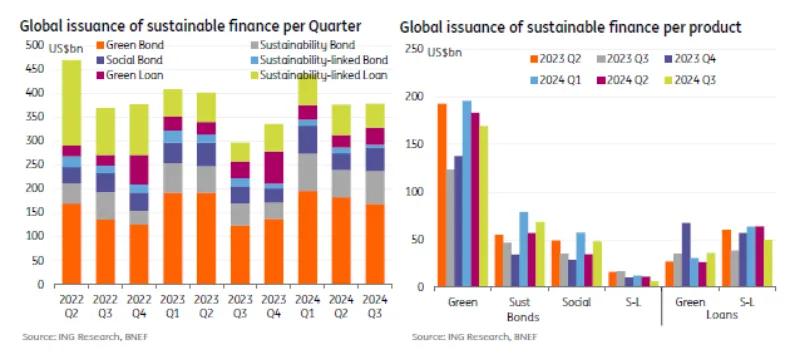

Sustainable finance issuance remained more on the low side in Q3 this year. Global sustainable issuance totalled US$385bn in Q3 2024, matching that of the rather low amount seen in Q2, both of which are lower than the quarterly average of a little over US$400bn. However, when compared to previous Q3 figures it is an increase on last year (which was particularly low) but is more in line with most other Q3s. Generally, supply is more concentrated in the first half of the year. As we saw a particularly busy Q1, the YTD number is still decent at US$1,259bn, which is up on last years' US$1,131bn, and in line with the US$1,265bn in 2022 and US$1,389bn in 2021.

The theme of slightly lower supply looks set to continue in Q4. In October just US$117bn of sustainable finance was issued. For November there has been more than normal limitations on issuance windows (for example the US elections), and December, as per usual, should be very quiet. This means Q4 supply will really struggle to match the levels seen in Q4 of the previous two years, which came in between US$340-380bn. We expect sustainable finance will be more plentiful next year in 2025, matching the rise of supply overall, but also as issuers turn towards ESG in order to increase demand and get a slightly lower cost on their new issues.

In Q3, the main drivers for lower global sustainable supply were the sustainability-linked debt products. Sustainability-linked bonds totalled just US$6.5bn in Q3, down substantially from the US$22bn quarter average. Sustainability-linked loans totalled just US$50bn in Q3, much lower than the US$95bn quarterly average.

Meanwhile the other debt products actually come in line or even slightly up on the quarterly averages, and average levels for Q3.

In Q3, global green bond issuance amounted to US$169bn, this is up slightly on the quarterly average of US$160bn, but this is also up considerably from the Q3 average seen over the past couple of years of just US$130bn. Sustainable bond supply reached a notable US$69bn in Q3, higher than the US$55bn quarterly average. Social bond issuance was pencilled in at US$48bn in Q3, up slightly up on the US$42bn quarterly average and up on the Q3 average for the past 3 years of US$38bn. Lastly then, the Green loan supply was mostly in line with the quarterly average and matches the amount seen in Q3 last year, pencilled in at US$36bn.

As per the norm, the largest amount of sustainable issuance comes in EUR and USD. In Q3, both EUR and USD sustainable finance totalled US$131bn each, in line with Q3 levels of 2021 and 2022, but is up on the rather low Q3 levels we saw in 2023.

Whilst corporates still remain the biggest issuers of sustainable finance, they did see a decrease in Q3 down to US$136bn, lower than that US$163bn quarterly average. Financials on the other hand, amounted to US$91bn, on par with the normal quarterly average. Sustainable government bond supply (Govies, Sov, Municipal and ABS) increased slightly in Q3, totalling US$159bn, up on the average US$143bn.

Jacomijn Vels, ING’s global head of sustainable finance:

This reflects the strongest Q3YTD performance since we started recording volume mobilised in 2022. We’ve seen growth across key regions where we’re active, supported by the extension of our Sustainable Finance presence in new markets

Deal highlight: Ramsay Healthcare

ING acted as Sole Sustainability Coordinator for the update and extension of AUD 1.7bn sustainability-linked facilities for Ramsay Health Care, one of the largest and most diverse private healthcare companies in the world. The refreshed KPIs relate to emissions, energy usage, on-site renewables, supplier sustainability performance and mental health training. A new Second Party Opinion was issued by DNV. Ramsay also developed a Sustainability Deed Poll, creating a common framework which can be applied across all future sustainability-linked financings, including derivatives and guarantees, allowing easier and more efficient access to the sustainability-linked structure over time.

Want to know more about our Sustainable Finance offering in Australia? Contact Opens in a new tabmichael.puli@ing.com

ING continues to deliver strong growth in 3Q24

ING sees a robust 3Q24 in terms of transaction numbers and volumes, mobilising sustainable financing of €28.6bn, reflecting a ca 6% increase compared to the same period last year. This adds to a positive 2024 position for ING, with the Q3YTD volume mobilised (€85.3bn) 16% ahead of the previous year.

We saw the increase in volume mobilised driven by sustainability-linked loans and green bonds. In addition to volumes from loans and bonds, we’ve also seen greater sustainable finance volumes in 2024 relating to commercial paper and guarantees, demonstrating our engagement with clients across a wider range of sustainable finance products.

While most of ING’s sustainable finance activities continued to come from EMEA (ca 70% of Q3YTD volumes), we have seen strong year-on-year growth across all regions including APAC and Americas. Strong growth in volume mobilised in Q3 from Americas and APAC, driven by sustainability-linked loans and green bonds, helped to offset a small reduction in EMEA volumes.

“We regularly engage with clients looking to access sustainable finance products for the first time as well as existing clients returning to the market. Notable and sizeable transactions by well-known corporates this year have provided a strong signal in support of the sustainable finance markets. We continue to see a healthy pipeline of transactions and we’re hopeful that the global sustainable finance market can return to growth in 2024”, states UK Head of Sustainable Finance, Arash Mojabi.

Looming ESRS to heighten focus on company disclosure

Meeting the European Sustainability Reporting Standards early will come with benefits in terms of quality of information, investor access, and ESG risk awareness.

In 2025, the first group of companies will start disclosing according to the European Sustainability Reporting Standards (ESRS) for the financial year 2024. These reporting standards apply to companies subject to the Corporate Sustainability Reporting Directive (CSRD). Initially only large public interest companies must disclose information on their ESG related impact, risks, and opportunities. But between 2026 and 2029 the reporting scope will gradually expand to all large companies, listed SMEs and EU branches and subsidiaries of non-EU companies.

With scrutiny on sustainability that has grown over time, corporates did not wait for the CSRD to start looking inward at their businesses and activities. Most large corporates have already put in place administrative units in charge of ESG information and have developed sustainability plans with mid to long term objectives. On top of what corporates publish themselves, more ESG KPIs and assessments are available on the market.

Towards data-driven monitoring in Sustainable Finance

Sustainability-linked products have been instrumental in advancing INGs ambition to accelerate the transition of our clients. These products aim to empower our clients to set and achieve ambitious sustainability goals on their most material ESG topics. As a leading player in this field, we leverage our extensive transaction experience to enhance our client dialogue. Additionally, we place significant value on the ongoing engagement with our clients who have issued sustainability-linked products, utilizing their annual performance updates against agreed sustainability targets.

In recent years we have been working on developing a monitoring framework for sustainable finance products. Whereas the purpose of this monitoring framework is primarily for internal purposes, we can share the aggregated analysis of the most frequently addressed topics in our recent sustainability-linked loans.

As anticipated, climate change is the predominant topic, reflecting the maturity of our clients’ climate-related target setting, particularly in reducing greenhouse gas emissions. Beyond climate change, the second most common focus is on our clients’ workforce, with key performance indicators (KPIs) primarily addressing diversity and inclusion, as well as health and safety.

ING & Climate

Society is transitioning to a low-carbon economy. So are our clients, and so is ING. We finance a lot of sustainable activities, but we still finance more that’s not. See how we’re progressing on Opens in a new tabour climate approach.

ING’s Sustainable Finance Pulse 5, a quarterly glimpse into the world of sustainable finance and ING’s take on it

ING Sustainable Finance Pulse - issue 5

ING Sustainable Finance Pulse - issue 5ING’s Sustainable Finance Pulse 3, a quarterly glimpse into the world of sustainable finance and ING’s take on it